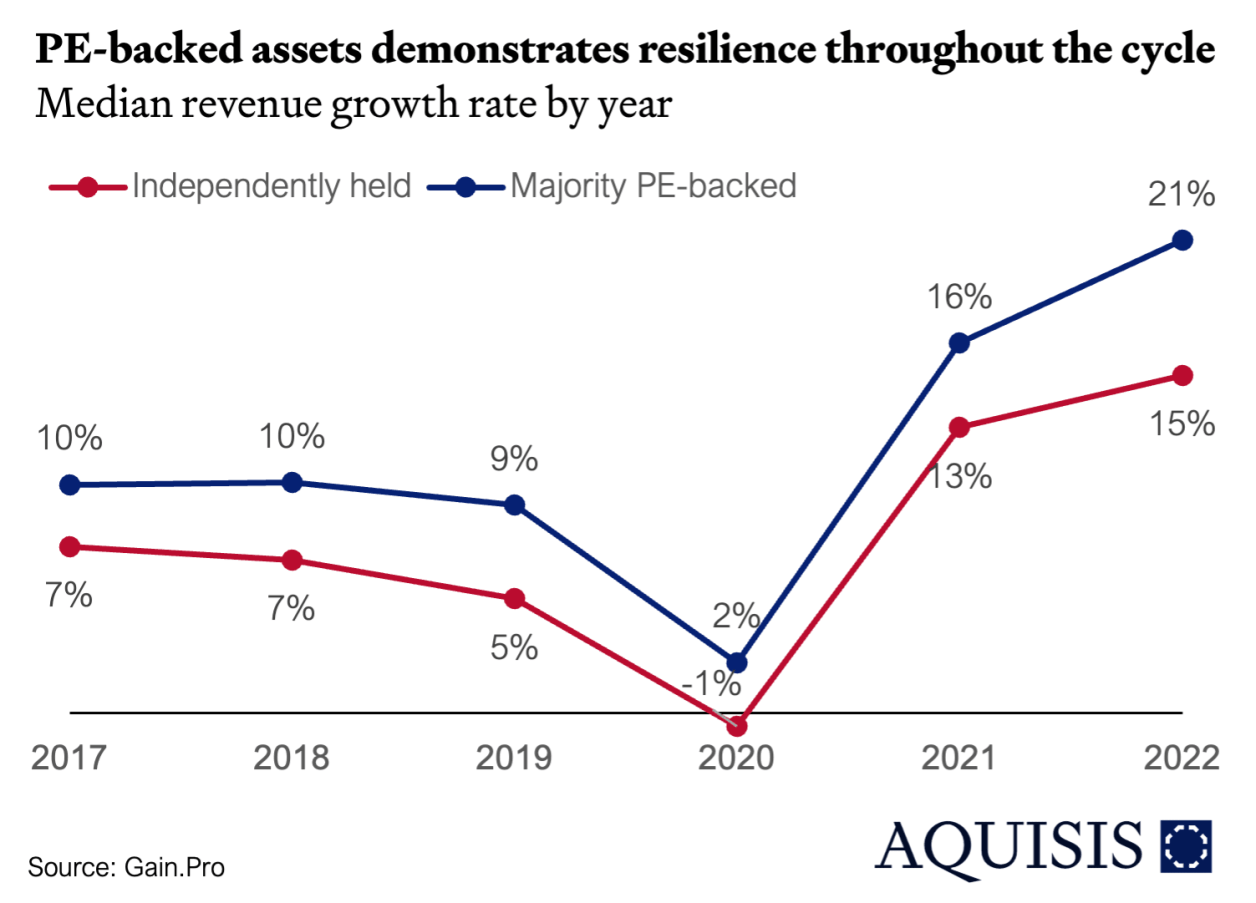

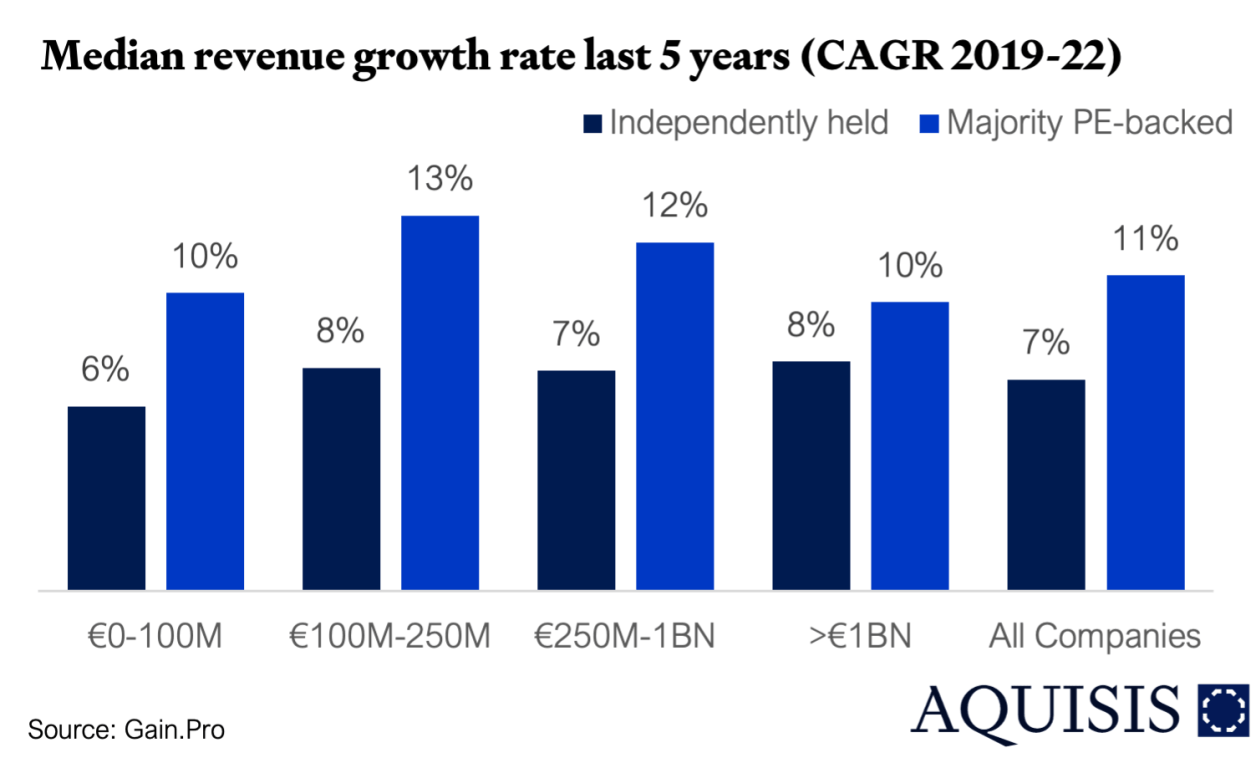

Research suggests that PE firms enhance total factor productivity, refine managerial practices, focus patenting activity and mitigate agency problems. Following a buyout, target companies experience a 50% greater increase in sales compared to comparable control firms (Cesare Fracassi, 2020). This trend holds true across businesses of all sizes. However, as companies grow larger (exceeding €1bn in revenue), the growth differential tends to diminish (Jani, 2024). This growth is primarily driven by an increase in sales volume rather than by price adjustments.

How do firms achieve this increase in units sold? First, PE-backed firms introduce more new products, significantly increasing the number of items ordered. Second, they innovate by entering new consumer categories. Finally, their products reach a broader audience by expanding into new stores, retail chains, and geographic regions. Private equity plays a key role in this process by providing access to financing, managerial expertise, and valuable business connections. These resources enable younger, private companies to expand their product lines and achieve more effective growth.